Many finance and accounting functions treat the existence of a signed document as sufficient evidence to support revenue recognition. From PSAK 115/IFRS 15 perspective, this assumption is incorrect and introduces a significant risk of material misstatement.

Under PSAK 115/IFRS 15, a signed agreement constitutes a “contract” for revenue recognition purposes only if all five criteria are satisfied. Failure to meet any single criterion precludes contract existence, requiring amounts received or billed to be accounted for as a liability rather than revenue. The resulting impact may include revenue reversals, material adjustments, financial statement restatements, and heightened audit and regulatory scrutiny.

Consider the following illustrative scenario:

A sales function executes a Memorandum of Understanding with a large enterprise customer to secure a strategic relationship. The agreement specifies that key payment terms are “subject to future discussion.” Based on the customer’s order, the production function commences manufacturing activities. From a technical standpoint, the absence of enforceable payment terms raises significant doubt as to whether the arrangement creates legally enforceable rights and obligations.

If the contract is not appropriately identified at inception, the entity risks recognizing revenue before a contract exists, recognizing revenue for an amount that is not fixed or determinable, or recognizing revenue based on assumptions that do not meet the legal and economic substance requirements of PSAK 115/IFRS 15.

In practice, Step 1—identifying the contract—is one of the most common root causes of material misstatements in revenue observed today. Contract identification forms the foundation of revenue recognition; when this foundation is flawed (that is, when the contract is incorrectly identified), all subsequent analyses built upon it are likely to fail.

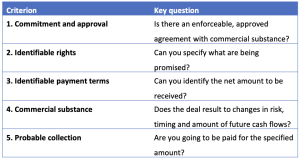

In accordance with PSAK 115/IFRS 15, an agreement qualifies as a contract only if all five criteria are met

Failure to meet any of the criteria precludes the application of PSAK 115/IFRS 15 15. As a result, revenue recognition may be deferred, potentially leading to a misstatement of performance to date. In accordance with PSAK 115/IFRS 15, an agreement qualifies as a contract only if all five criteria are met.

Our expertise helps transform contract-related risk into accounting clarity by applying the five criteria as a structured framework for contract identification.